|

• The FAO’s world food commodity prices index remained largely unchanged in August, leaving the index 6.9% higher year on year. Increases in meat, sugar and vegetable oil prices offset declines in cereal and dairy quotations. The Meats increased by 0.6% in August, reaching a new all-time high, underpinned by strong demand in the US and China. The sugar index rose slightly, by 0.2%, after five consecutive declines. Concerns over Brazilian sugarcane production an stronger global import demand were partially countered by prospects for larger crops in India and Thailand. Vegetable oils (+1.4%) reached the highest price level in over three years, led by palm, sunflower and rapeseed oil quotations. Decliners in August included cereal prices (-0.8%) amid dropping wheat prices and fierce competition pushed down Indica rice prices. Dairy prices declined by 1.3%, with butter, cheese and whole milk powder quotations down amid subdued import demand from key Asian markets.

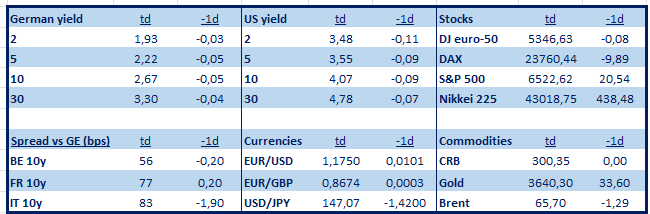

• Canadian employment fell in August and missed expectations in doing so. Around 65.5k jobs were lost, marking the first back-to-back decline (-41k in July) since 2020. Part-time jobs bore the brunt (-59.7k). The unemployment rate rose 0.2 ppts to 7.1% – the highest since in four years – and the participation rate eased slightly to a 3.5 year low at 65.1%. Employment decreased across several industries, led by professional, scientific and technical services (-26k), transportation and warehousing (-23k), and manufacturing (-19k). The report fuels speculation for another rate cut by the Bank of Canada. Market implied odds picked up from 57% yesterday to 79%. The central bank kept rates steady at 2.75% for three consecutive meetings but never shut the door for future downward adjustments. CPI numbers due one day ahead of the BoC meeting (Sep 17) will decide over the matter. USD/CAD whipsawed amid a weak US labour market report but currently trades unchanged around the pre-payrolls 1.38 levels. The Loonie does lose out sharply against all other G10 peers.

|

0 Comments